The PAGA Trap: Why “Zombie Policies” and the Exempt Illusion Are About to Bankrupt You

If you walked into your office today and saw a “Zombie,” a creature that is technically dead but still stumbling around causing havoc, you would probably do something about it. Yet, most California businesses are crawling with them.

I’m talking about Zombie Policies.

A Zombie Policy is a rule that lives in your employee handbook (undead & ignored) but is completely disregarded in daily operations. It’s the rule that says “All overtime must be pre-approved,” even though your managers routinely wave through unapproved hours. It’s the policy that says “30-minute uninterrupted meal period breaks are mandatory before the end of the 5th hour worked,” even though your team eats at their desks or takes only 25 minutes before jumping back to answer a client call.

In many states, a Zombie Policy is just poor management. In California, a Zombie Policy is a plaintiff attorney’s favorite weapon.

This is not just about sloppy handbooks. It is about the single biggest financial risk facing California employers today: The Misclassification of the “Exempt” Professional.

The “Exempt” Illusion: A Multi-Million Dollar Lie

Many modern firms operate on a dangerous assumption: “If I pay them a good salary and call them a ‘Consultant’ or ‘Manager,’ they are Exempt.”

They build their entire business model on this. They mandate 47.5-hour work weeks. They set billable hour quotas that require 47.5+ hours of desk time. They burn people out and assume they are immune to overtime laws because the employees are “White Collar Professionals” with college degrees, certification, and years of experience.

Strategic Realism: You aren’t immune. You are a target.

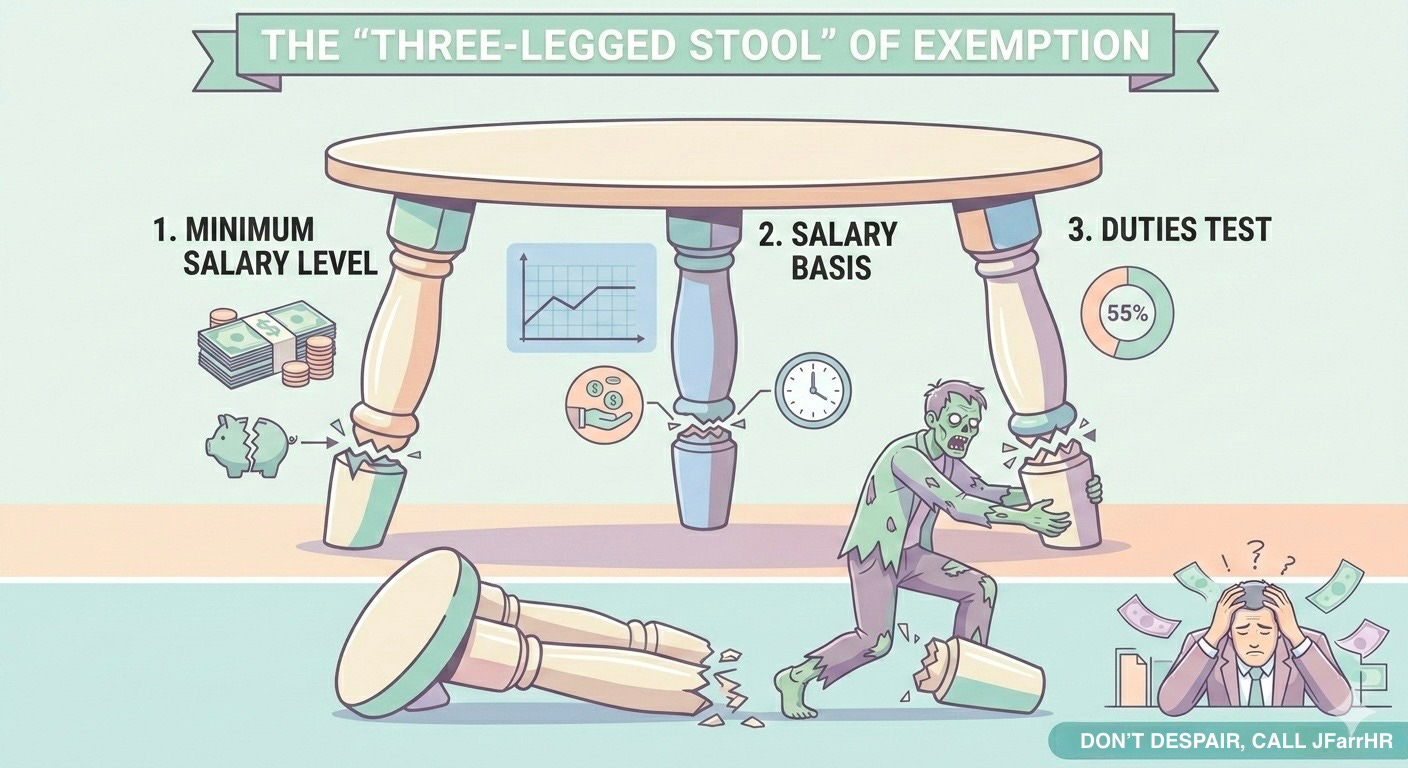

The “Three-Legged Stool” of Exemption

Before we look at the wreckage of companies that got it wrong, you need to understand the math. In California, an “Exempt” status isn’t a suggestion; it’s a three-legged stool. If one leg breaks, the whole thing collapses, and you are back to owing overtime, meal break premiums, interest, etc.

To maintain the exemption, you must satisfy all three of these criteria simultaneously:

The Salary Level: As of January 1, 2026, the minimum salary for exempt employees in California is at least $70,304/year which is based on the statewide minimum wage rate. Many California cities and counties have enacted ordinances which establish minimum wage rates that are higher than the statewide requirement and are implemented throughout the year. If you make a mistake and pay a dollar less than the specific ordinances specify, the stool breaks.

The Salary Basis: The employee must receive a predetermined amount that does not fluctuate based on the quality or quantity of their work. If you dock pay for a 4-hour absence or pay “straight time” for extra hours, the stool breaks.

The Duties Test: This is where most “Zombies” hide. The employee must spend more than 50% of their actual work time on exempt tasks (discretion and independent judgment on matters of significance). If the reality of the job forces them into grunt work for 51% of their day, the stool breaks.

The “No Records” Nightmare: A 4-Year Lookback

If one leg of that stool breaks, you don’t just owe overtime. You face a much more expensive problem: The Missing Time Records.

When you classify an employee as Exempt, you stop tracking their meal and rest breaks. If that classification is later found to be wrong, that lack of data becomes your death warrant.

Under California’s Donohue standard, if your time records are missing or non-compliant, the courts recognize a “rebuttable presumption” that no breaks were provided. Since you have no records to prove otherwise, you are effectively guilty until proven innocent.

This triggers two separate penalties for every single day worked:

1 Hour of Pay for the missed Meal Period.

1 Hour of Pay for the missed Rest Break.

That is two hours of “Premium Pay” per day, calculated at the employee’s “Regular Rate of Pay” (not just their base salary). Multiply that by 4 years (the statute of limitations under California’s Unfair Competition Law), and your “Exempt” manager just became your most expensive hourly liability.

Here are four specific case studies — backed by California case law — that prove why your “Exempt” workforce might actually be a massive, unpaid liability. And why you should care sooner rather than later.

Case Study 1: The “Unrealistic Expectations” Trap

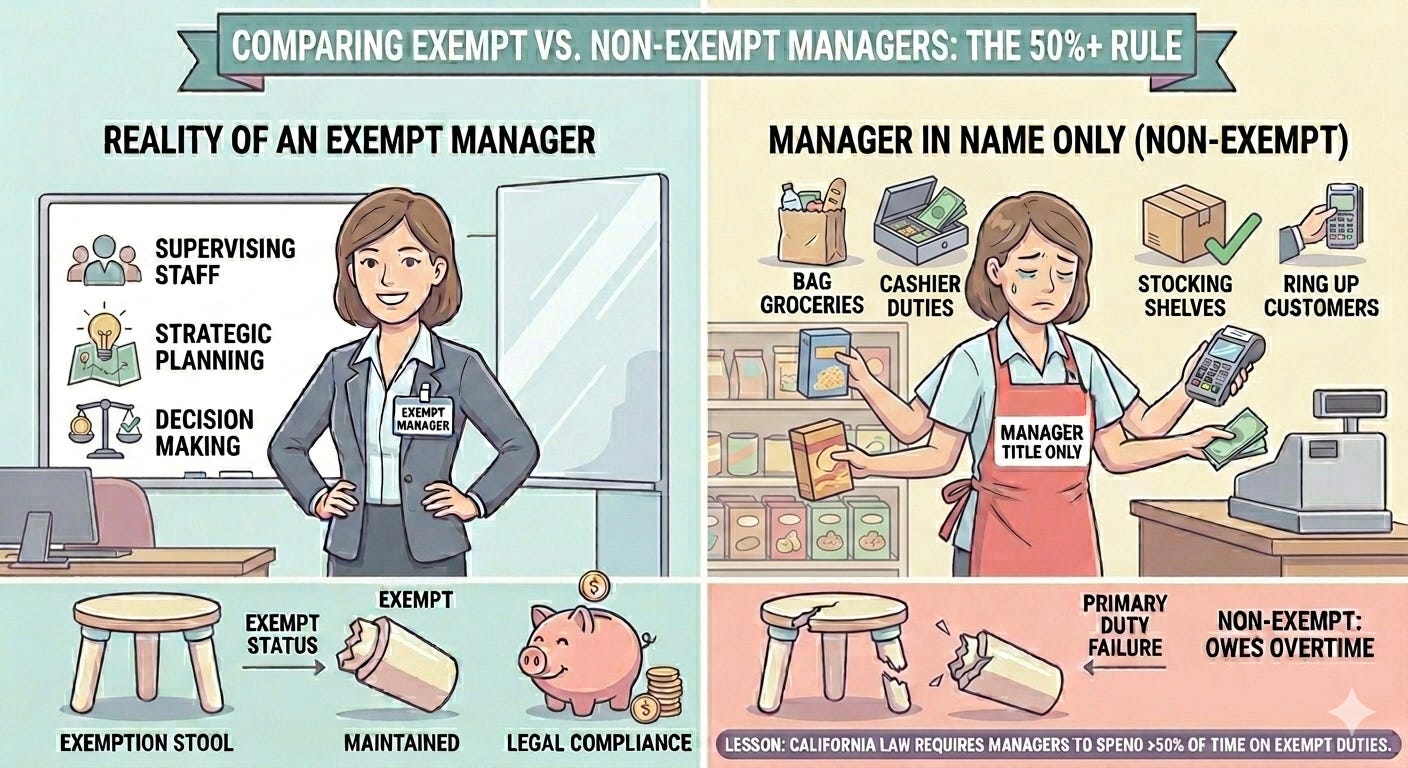

The Precedent: Heyen v. Safeway Inc. (2013)

The Scenario:

Safeway classified Linda Heyen as an Exempt “Assistant Manager.” Her job description was full of leadership language: “Managing the store,” “Supervising staff,” “Operational oversight.”

The Reality:

Safeway, like many modern employers, ran a “Zero Slack” operation. The labor budget was so tight that to keep the store running, Heyen had to spend the vast majority of her time bagging groceries and stocking shelves. She argued she was essentially a highly paid bagger.

The Ruling:

The court sided with Heyen. They ruled that Safeway’s “expectations” for her to be a manager were unrealistic given the actual labor budget. Because the reality of the job required her to do the same grunt work as the people she “supervised” more than 50% of the time, she was actually non-exempt. Safeway was ordered to pay her $26,184.60 in unpaid overtime (plus interest).

The Lesson:

$26k might sound manageable for one employee. Now multiply that by every California “Manager” you have.

It’s worth emphasizing here that California is a “quantitative” state. Federal law looks at the “primary duty” (qualitative), but California requires more than 50% of the time to be spent on exempt tasks. If you mandate a 47.5-hour week but don’t provide enough support staff, and your exempt “Consultants,” “Business Partners,” and “Generalists” end up doing data entry, following SOPs, and filing over half the time, you lose the exemption. You owe them overtime for every minute of that “admin,” non-exempt level work.

Case Study 2: The “Cookie Cutter” Class Action

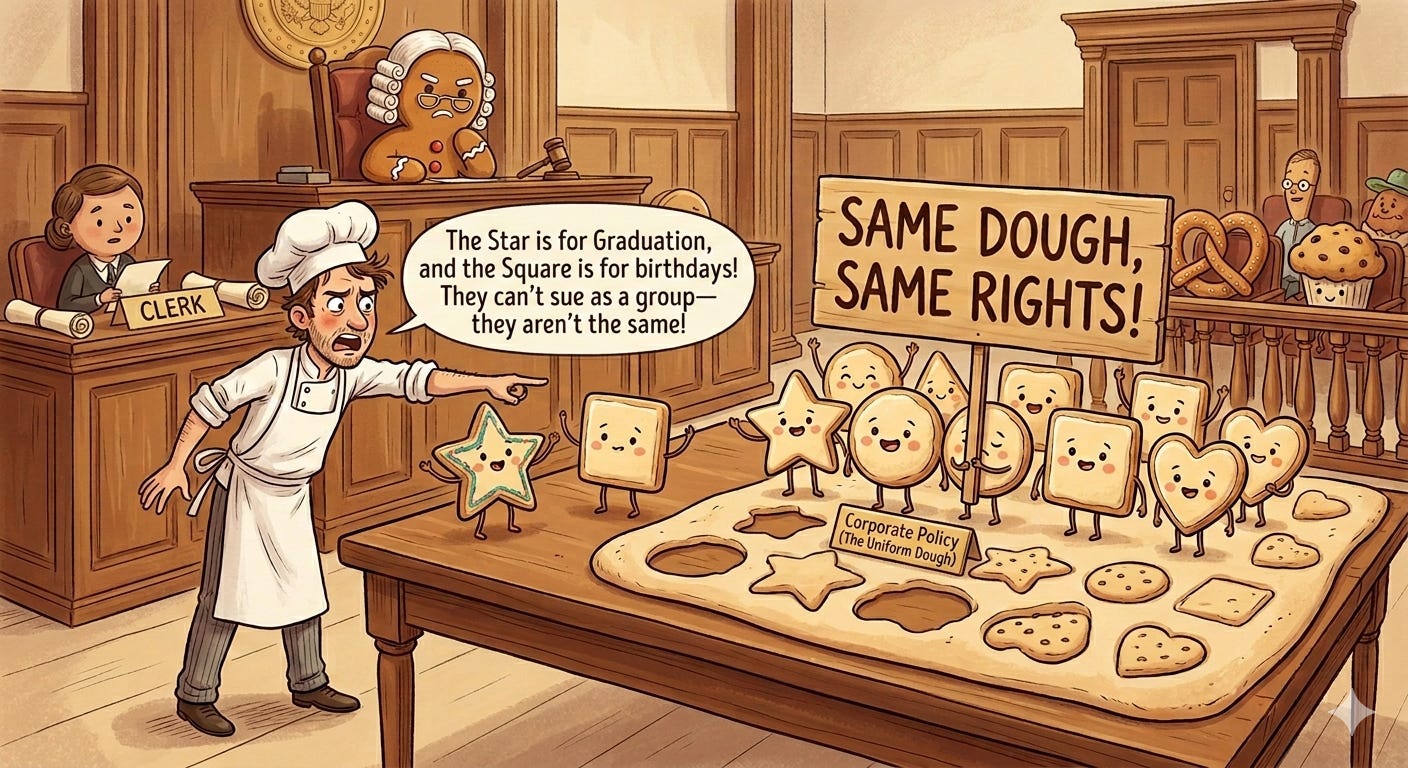

The Precedent: Martinez v. Joe’s Crab Shack Holdings (2014)

The Scenario:

A group of managerial employees sued, claiming misclassification. The company argued that a Class Action was impossible because every manager’s day was different. “You can’t sue us as a group,” they argued, “because Manager A did more cooking, and Manager B did more scheduling.”

The Ruling:

The court allowed the Class Action to proceed. Why? Because the policies were uniform. The manager employees successfully argued that corporate set strict, uniform labor budgets that forced all managers to fill in as cooks.

The Lesson:

If you have a “Zombie Policy” in your handbook that mandates a strict schedule for all Exempt staff, you have just handed a plaintiff attorney the glue they need to certify a Class Action. You aren’t fighting one lawsuit; you are fighting 500.

Case Study 3: The “Hourly Exempt” Trap

The Precedent: Negri v. Koning & Associates (2013)

The Scenario:

An insurance adjuster was classified as Exempt but was paid based on the hours he worked. He had no guaranteed minimum salary floor; if he didn’t work, he didn’t get paid.

The Ruling:

The court ruled that if you calculate pay based on hours worked without a guaranteed floor, the exemption is destroyed.

The Grey Area Risk:

Many Consulting & Outsourcing firms sit in a dangerous risk zone here. They pay a salary, but they track time like a factory. If you require Exempt staff to log every 15 minutes of work performed, highlight “under-hours” in red, and threaten discipline for working 44 hours instead of 47.5, you are providing evidence that you treat them as hourly workers. If it walks like a duck and clocks in like a duck... The California courts will make you pay it like a duck.

Practice Notes: Even if they only work 40 hours, if they don’t meet California’s Duties Test, you still owe penalties for missed meal/rest breaks, inaccurate wage statements, and if after termination, waiting time penalties.

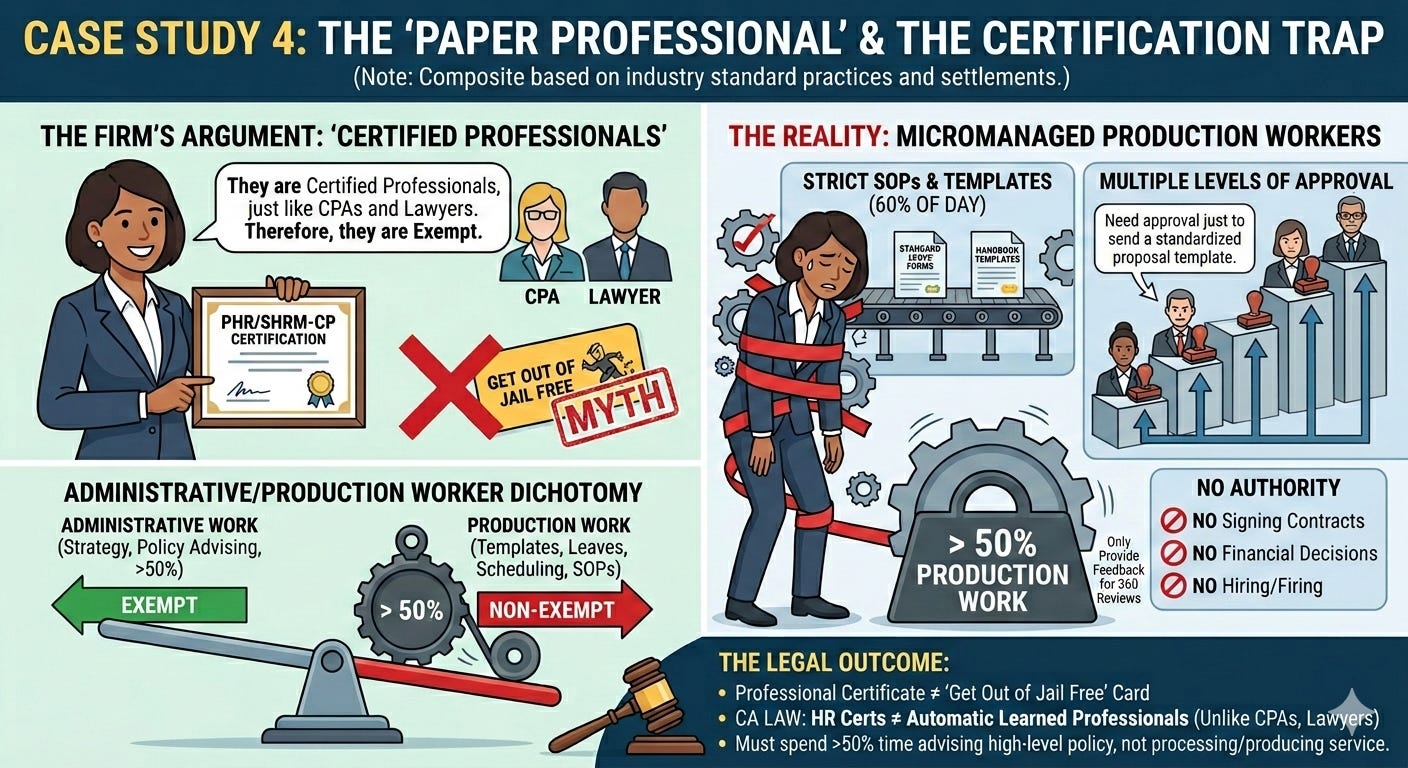

Case Study 4: The “Paper Professional” & The Certification Trap

(Note: This is a composite of industry standard practices and settlements and not one actual case.)

The Scenario:

A national Outsourcing & Consulting firm hired “HR Business Partners” to provide guidance to clients. To justify the Exempt status, the firm required every hire to hold a professional certification (PHR, SPHR, SHRM-CP, etc.) within six months of hire or face termination.

The firm argued: “They are Certified Professionals, just like CPAs and Lawyers. Therefore, they are Exempt.”

The Reality:

Despite the fancy titles and certifications, these Business Partners were micromanaged by the firm:

They followed strict Standard Operating Procedures (SOPs) for 60% of their day and provided clients standard templates produced by the firm.

They needed a minimum of one (and up to five) levels of approval just to send a proposal template with standardized service fees to a client.

They had no authority to sign contracts or commit the firm to any financial decisions.

They had no authority to hire or fire, only to provide “feedback” on performance in a verbal 360-style performance review process with management, peers, and coworkers.

The Outcome: The Certification Myth

In similar litigation, courts have repeatedly found that a professional certificate is not a “get out of jail free” card for employers. While California law recognizes doctors, teachers, engineers, CPAs, and lawyers as Learned Professionals, it does not grant the same automatic status to HR certifications like the PHR or SHRM-CP.

Most HR roles must instead qualify under the Administrative Exemption, which can lead to a specific legal trap for consulting firms known as the Administrative/Production Worker Dichotomy.

In California, the law distinguishes between “administering” the business and “producing” the product. If your firm sells HR services, and your “Business Partners” are merely producing that service (processing leaves and drafting handbooks via SOPs), courts often classify them as “Production Workers” rather than Administrators.

To maintain the exemption, they must spend more than 50% of their time actually advising on high-level management policy (strategy). If they are bogged down with ‘production’ work for even 51% of their week — tasks like data entry, scheduling, following Handbook SOPs, or providing clients policy templates they did not create — the exemption evaporates.

The Misclassification Trap

Misclassification happens when a role shifts from strategic to clerical. If your HR Business Partner is primarily:

Following a Standard Operating Procedure (SOP) to process a leave of absence.

Entering data into a “Handbook Wizard” to generate a template.

Applying established company techniques rather than independently creating or advising on policy strategy.

Then, under California’s quantitative rule, they are likely non-exempt. In the eyes of the DLSE, they aren’t a “Business Partner,” they are a “Process Follower.” One firm learned this the hard way, settling a single-plaintiff “Business Partner” claim for over $450,000 in unpaid overtime and penalties because they micromanaged a professional into a clerical corner.

The lesson is simple: In California, you don’t pay for the letters after the name; you pay for the autonomy you actually allow them to exercise.

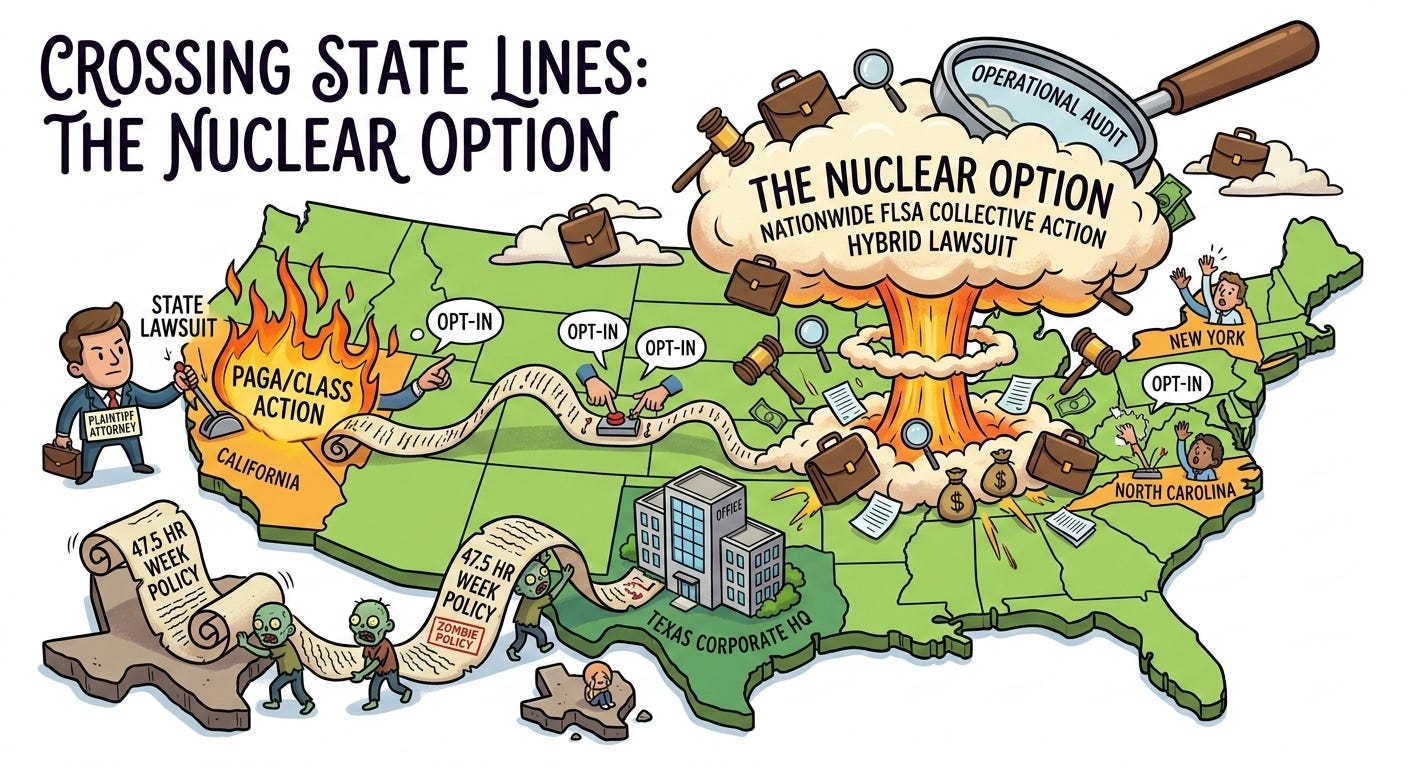

The “Nuclear Option:” Crossing State Lines

If your Zombie Policies are written by corporate HQ and applied nationally, you have a bigger problem than California.

Plaintiff attorneys are now filing “Hybrid” Lawsuits.

They file a state PAGA claim or Class Action for your California employees and simultaneously file a Federal FLSA Collective Action for your employees in other states.

Suddenly, that “Mandatory Scheduled 47.5 Hour Week” policy you wrote in Texas isn’t just a local problem. It allows employees in your North Carolina, New York, and Nevada offices to “opt-in” to the federal lawsuit. (Keep in mind, many states like NY & NV have their own high-salary thresholds that often dwarf federal standards.) You aren’t just facing a state penalty; you are facing a nationwide operational audit.

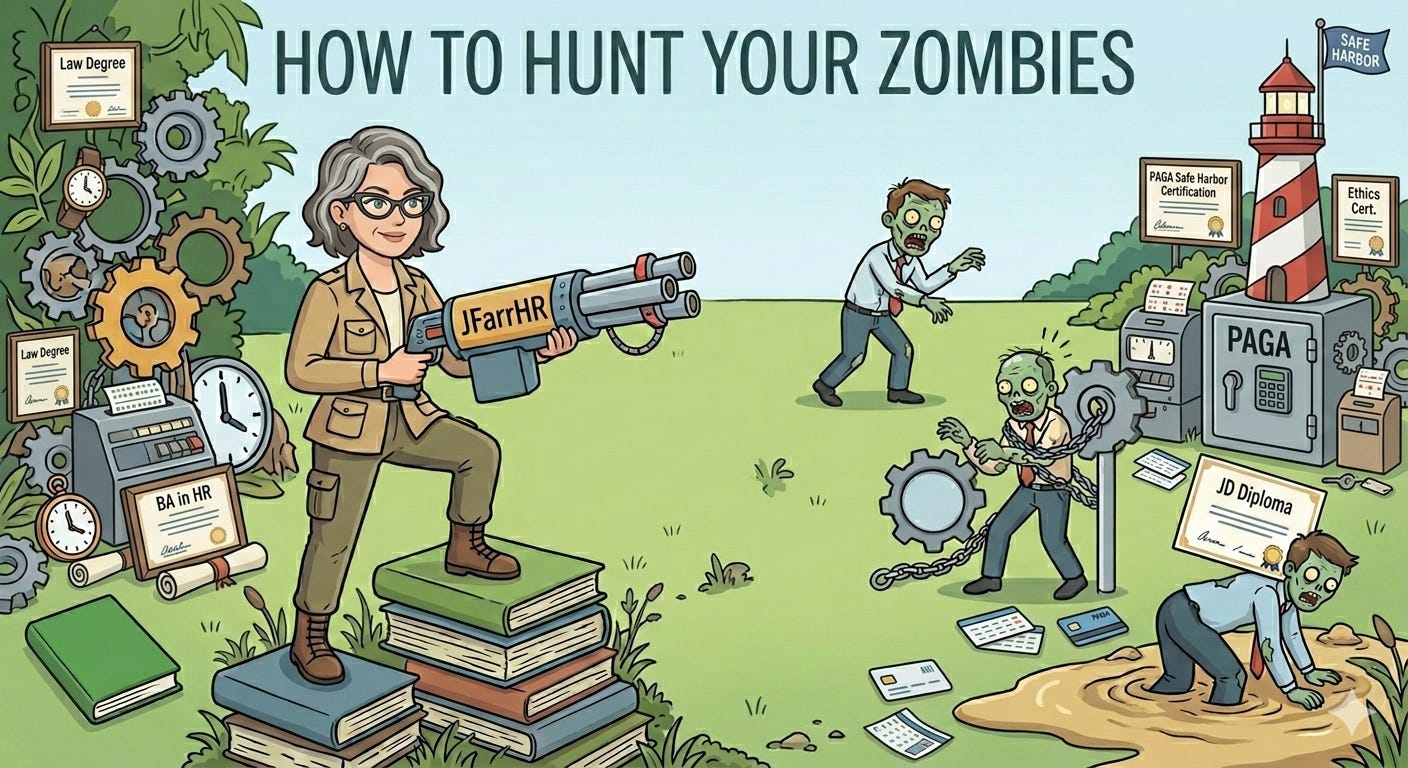

How to Hunt Your Zombies

You need to conduct a “Reality Audit” of your handbook and your job descriptions. Sit down with your managers and ask these three questions about every “Exempt” role:

1. “Does the Calendar Match the Handbook?”

If your handbook says “Exempt,” but your calendar and/or time records show you tracking their every move (except break and meal periods), you have a problem.

2. “Is the ‘Discretion’ Real?”

Can this employee sign a $500 contract without asking permission? Can they deviate from the SOP if a client needs it without having to get anyone’s approval? If the answer is “No,” they are likely non-exempt.

3. “Are we relying on a Certificate?”

If your only defense for their exemption is “They have a SHRM-CP and a Bachelors Degree” call your lawyer. You are standing on quicksand.

The Realist Bottom Line

Your employee handbook is not a wish list. It is a legal contract that defines your defense in court. If your policies don’t match your practices, you aren’t just being disorganized. You are handing the opposing counsel their closing argument.

But there is hope.

Proactive audits now offer a ‘Safe Harbor’ under the PAGA reforms. By fixing these ‘Zombies’ before you get a plaintiff’s notice, you can reduce your penalty exposure by up to 85%. In California, ignorance is expensive, but proactivity is a massive discount. Under the new law, the clock starts ticking the moment you realize there’s a problem — don’t let a plaintiff’s attorney be the one to tell you.

Is your workforce truly Exempt? Or are they just “Paper Professionals”?

Let’s schedule a Free Consultation to get a handle on where things stand. We specialize in Compliance Reality Checks where we can review your core policies, identify the Zombies, and get your operations PAGA-proofed before the next audit.