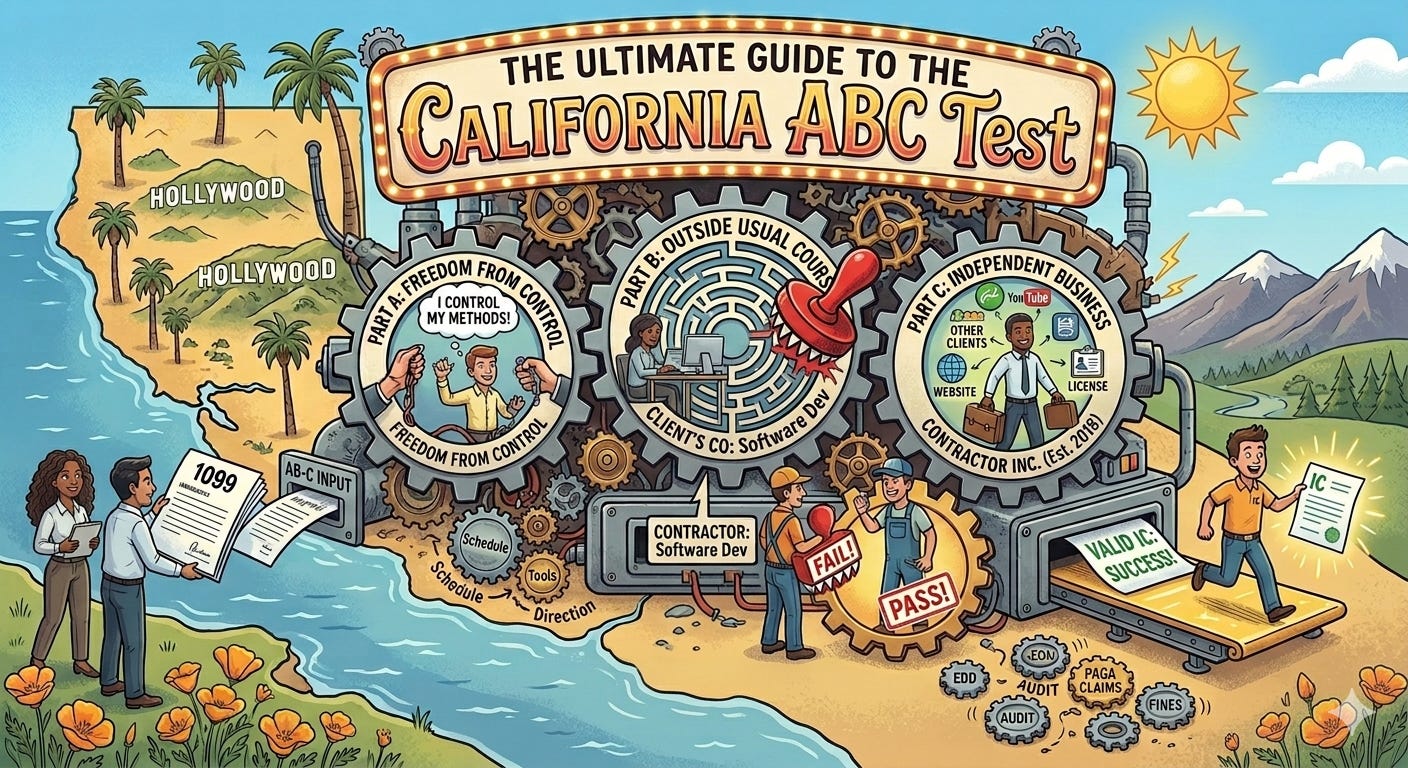

The Ultimate Guide to the California ABC Test

How to Stop Gambling with Your 1099s

On Tuesday, we talked about the worst-case scenario: an out-of-state company getting hit with a forensically savage EDD audit because they tried to “1099” their way out of California red tape.

The post-audit bill for that single Sales Director mistake? $100,000+.

The reaction I usually get when I lay this out for a client is panic. The next question is always, “Okay, JFarr, you’ve properly terrified me. But how do I actually know if my contractors are legal?”

You don’t guess. You don’t use “common sense.” And you absolutely do not use the old test (Borello) that relied on “how much control you have.”

You use the ABC Test.

Strategic Realism: The Burden of Proof is on YOU.

In California, the law presumes that a worker is an employee. It is up to you, the employer, to prove otherwise.

To legally classify someone as a 1099 Independent Contractor, you must prove ALL THREE of the following conditions (A, B, and C) are met. If you fail even one, they are an employee.

Here is your Deep Dive audit checklist.

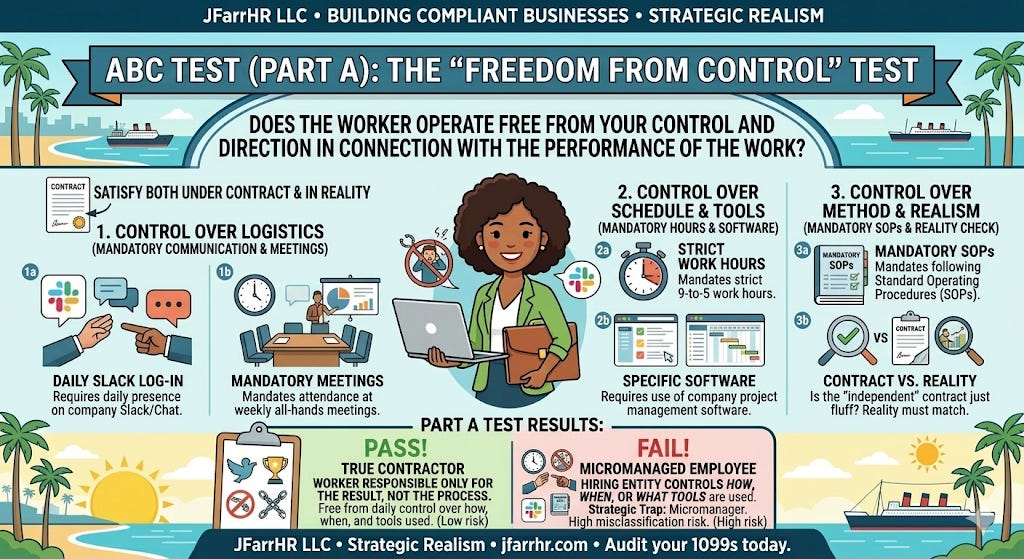

PART A: The “Freedom from Control” Test

The question: “Does the worker operate free from your control and direction in connection with the performance of the work?”

You must satisfy this test both under the contract and in reality.

Strategic Trap: The Micromanager. You have a contract that says they are “independent,” but you require them to log in to your Slack, work from 9-to-5, attend your weekly all-hands meeting, use your specific project management software, and follow your mandatory SOPs (Standard Operating Procedures).

Verdict: FAIL. If you control how they work, when they work, or what tools they use to work, they are an employee. A true contractor is only responsible for the result, not the process.

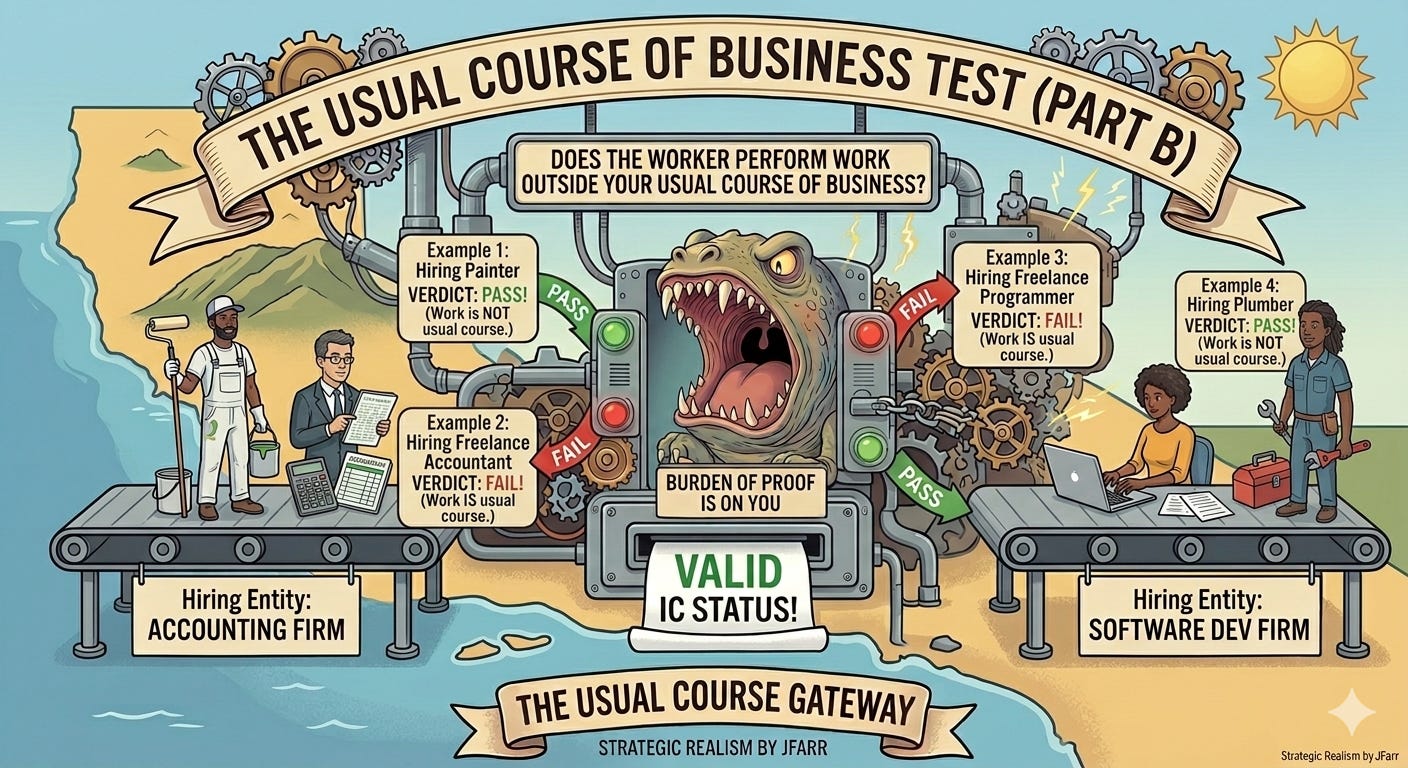

PART B: The “Usual Course of Business” Test (The Killer)

The question: “Does the worker perform work that is outside the usual course of your hiring entity’s business?”

This is where almost every single California business fails. This one rule effectively ended the gig economy for core operations.

Strategic Trap: The Core Operative. If you run a Software Development Firm and you hire a “Freelance Software Developer” to help your team build apps, you have failed Part B. Software development is what you do. Any developer working for you is an employee.

Verdict: FAIL. If the worker is producing the same “product” or delivering the same “service” that your company sells to clients, they are an employee. There is no loophole for this.

The Exceptions (What Passing Looks Like):

You pass Part B when the work is completely unrelated to your core mission.

• An Accounting Firm hiring a Painter to paint the office. (Passing)

• A Software Firm hiring a Plumber to fix a leaky sink. (Passing)

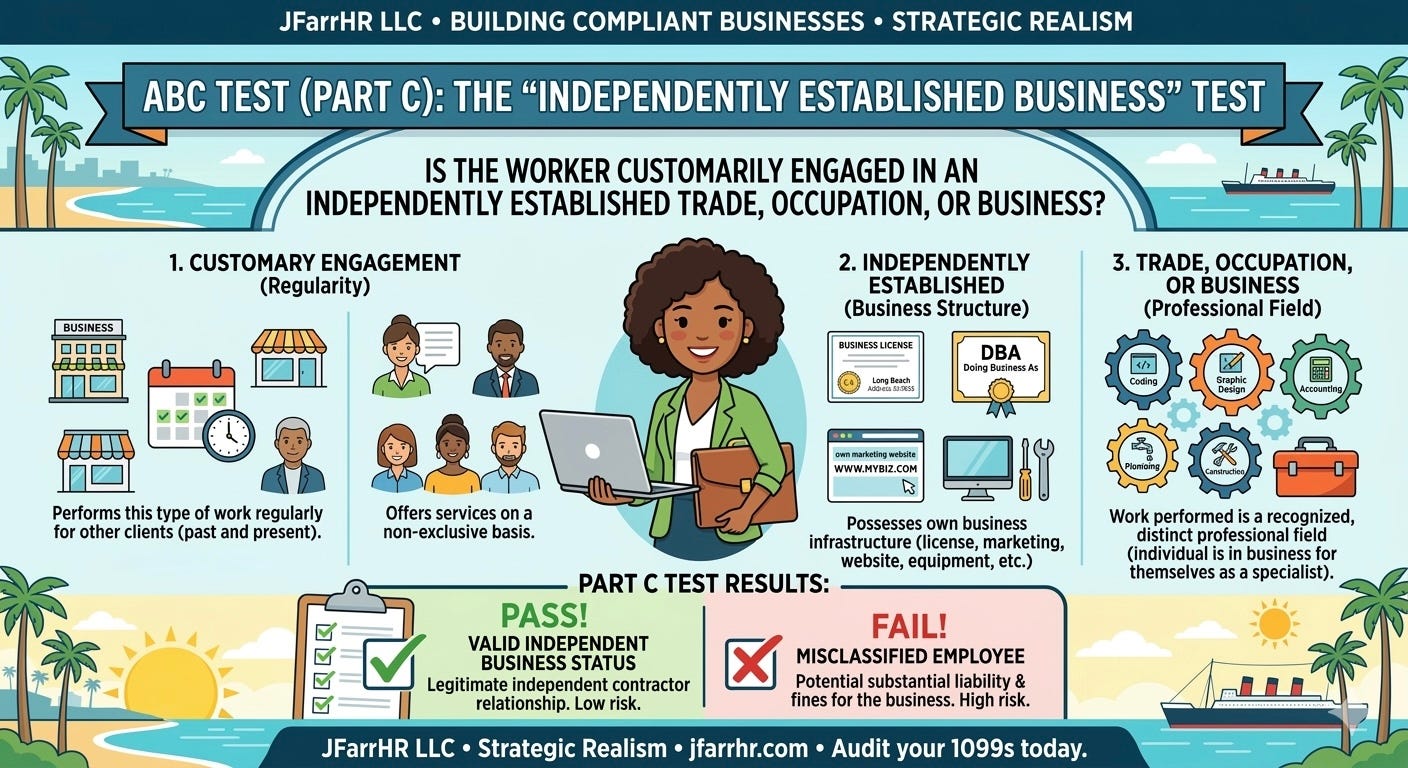

PART C: The “Independently Established Business” Test

The question: “Is the worker customarily engaged in an independently established trade, occupation, or business?”

This test ensures that the worker is truly in business for themselves, not just dependent on you for survival.

Strategic Trap: The 40-Hour-a-Week ‘Freelancer.’ You have a contractor who works only for you, has zero other clients, has no business license, no website, and no professional liability insurance. They may also be using your equipment (Part A fail).

Verdict: FAIL. The EDD does not see a business; they see a dependent employee who is lacking workers’ comp and payroll protection. To pass Part C, the worker must prove they have an established business independent of their relationship with you.

Addressing the Myth: “But It’s a B-to-B Relationship! They have an LLC!”

This is the myth that gets employers in the most trouble. They believe that if the contractor is an LLC, an S-Corp, or has a registered DBA, they are automatically exempt from the ABC test.

Strategic Realism: Having an LLC is not a “Get Out of Jail Free” card.

There is a specific exemption for true “Business-to-Business” (B-to-B) contracting relationships, but it is incredibly narrow. If you try to use it, you must meet 12 distinct criteria, including:

The business must be free from your control (Part A).

They must have a valid business license.

They must advertise to and have other actually existing clients (Part C).

They must perform services directly to you, not to your clients (This is crucial: If you hire an LLC to deliver services to your client, they are your employee).

You are almost never “safe” simply because you are contracting one business entity to another. If they fail the spirit of the ABC test, the state will find they are an employee.

Your Strategic Realism Audit (The Cleanup)

If you are an HR leader, a CFO, or an out-of-state founder with contractors in California, sit down this afternoon with a spreadsheet of every 1099 you have. Ask these three questions:

“Am I managing their process, or just waiting for the result?” (If process, you fail Part A).

“Does this contractor do what we do?” (If yes, you fail Part B).

“If I terminated this relationship today, would they lose 100% of their income?” (If yes, you fail Part C).

If you failed any of those questions, you need to transition those workers to employee status immediately.

Stop gambling with your company’s future on a misclassification risk. The state has an operational memory of 3 years of back taxes, penalties, and fines.

Get it right before they come looking.

Need Help Auditing Your 1099s?

Misclassification is one of the single biggest operational risks for California employers. If you are unsure if your “Freelance Team” is actually a “Forensic Liability,” we can help.

We offer a confidential 1099 Risk Audit, analyzing your contracts and your workforce duties against the ABC Test. We will give you a “Strategic Realism” roadmap to convert or restructure your workforce before an audit is launched.