The “What Now?” Guide to Worker Misclassification in California — Part 1

Part 1: The Price Tag of Panic

Part 1: The Price Tag of Panic

You read our guide on the California ABC Test. You sat down with your spreadsheet of 1099 contractors. You asked the hard questions about control, core operations, and independent business status.

And then, the panic set in.

You realized you failed Part B. Your “freelancers” are doing the exact same work your company sells. Or maybe you looked at your Exempt roster and realized your salaried “managers” are spending 80% of their day doing non-exempt, front-line tasks. The gap between realizing “we messed up” and figuring out “how do we legally and culturally fix it” is massive.

So, what now?

The answer isn’t as simple as, “Just flip them to a W-2 and tell them they get PTO now!” Changing a payroll status isn’t a strategy; it’s a reaction. Before you can fix the misclassification, you have to understand exactly what it is costing you.

Welcome to the Strategic Realism of cleaning up a classification mess. Over this four-part series, we are going to look at the financial fallout, the legal risks of making a transition, the scripts you need to use, and how to manage the operational culture shock.

First up: Let’s look at the math.

The Compounding Cost of Getting It Wrong

Leaders often underestimate the compounding nature of California labor code violations. When you misclassify a California worker — either by treating an employee as a 1099 contractor or a non-exempt worker as an exempt salaried employee — you aren’t just missing out on a few payroll taxes. You are stacking penalties, premiums, and back wages on top of each other.

Let’s look at what this actually looks like in practice.

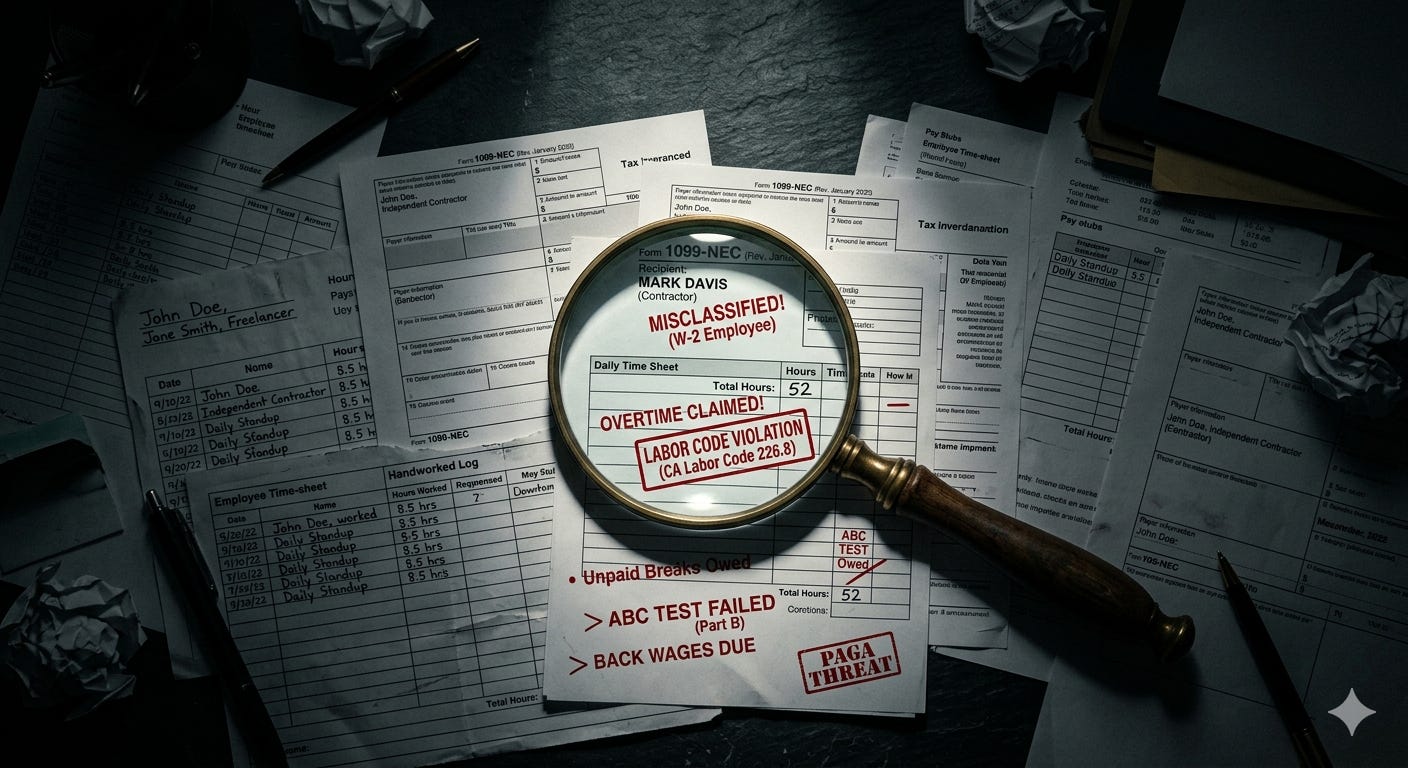

Case Study 1: The Accidental Pattern (1099 Misclassification)

Imagine a mid-sized marketing firm that hires five out-of-state “freelance” account managers. The firm requires them to attend daily stand-ups, use company email addresses, and manage the firm’s core clients. They are clearly employees under the ABC test, but they’ve been paid as 1099s for three years.

If one of those account managers files a claim with the EDD or a plaintiff’s attorney, the audit doesn’t just look at unpaid taxes. Here is the math:

Willful Misclassification Penalties: Under Labor Code Section 226.8, the state can levy civil penalties of $5,000 to $15,000 per violation. If they find a “pattern and practice” (which having five identical 1099s absolutely is), that penalty jumps to $10,000 to $25,000 per violation.

Unpaid Overtime & Minimum Wage: California has a 3-to-4-year lookback period under the Unfair Competition Law. Every hour worked over 8 in a day or 40 in a week over those years is owed at time-and-a-half.

Missed Meal and Rest Breaks: Because these workers were treated as contractors, they never clocked out for lunch. The company owes one hour of premium pay for every missed meal break and every missed rest break, every single day, for years.

Inaccurate Wage Statements: Under Section 226, failing to provide a compliant pay stub (because you were cutting a vendor check) carries penalties up to $4,000 per employee.

Expense Reimbursement (Section 2802): Did those contractors use their own laptops, cell phones, and home internet? The employer is legally required to reimburse all necessary business expenses.

Case Study 2: The Title-Only Manager (Exempt Misclassification)

Now, let’s look at the other side of the coin. You have an “Assistant Manager” who is paid a $70,000 salary and classified as Exempt. But when you audit their actual duties, they spend 70% of their day ringing up customers, stocking inventory, and covering the floor.

Job titles offer zero legal protection. In California, exemption is based on the actual daily duties performed. If they spend more than 50% of their time on non-exempt tasks, they are non-exempt.

The Fallout: When this employee realizes they are misclassified, the employer is suddenly on the hook for three to four years of unpaid overtime. If they worked a 50-hour week, that is 10 hours of time-and-a-half every week for over 150 weeks, plus the same compounding meal, rest break, and pay stub penalties mentioned above.

The Ultimate Multiplier: The PAGA Threat

If those numbers aren’t terrifying enough, we need to talk about the Private Attorneys General Act (PAGA).

PAGA is the mechanism that should keep leaders awake at night. It deputizes one single disgruntled misclassified worker to step into the shoes of the state and sue the company for labor code violations on behalf of all aggrieved employees.

The Strategic Realism: PAGA turns a localized, single-employee dispute into a company-wide forensic audit. The penalties are steep, and 75% of those penalties go directly to the state, with the remaining 25% distributed to the employees. Because plaintiff’s attorneys can recover their massive legal fees in these suits, PAGA claims are incredibly lucrative for them to pursue. You aren’t just fighting one contractor; you are fighting a state-sponsored class action.

What Now?

You cannot budget for a fix until you understand the liability. The “savings” you thought you were getting by utilizing 1099s or leaning on salaried managers are almost always wiped out tenfold by a single audit or PAGA claim.

But hope is not a strategy. Now that we understand the financial reality, we have to look at how to actually fix it.

In tomorrow’s Part 2, we are going to open up the “Make Whole” Menu. We will look at the legal and practical ways to transition these workers — from the quiet, prospective W-2 pivot to formal settlement agreements — so you can make an informed, grown-up business decision about your risk.

Need to audit your workforce before the state does it for you? Reach out to JFarrHR LLC for a confidential Risk Audit and a Strategic Realism roadmap to get your house in order.